Why most deposit claims are over-claims

Short answer

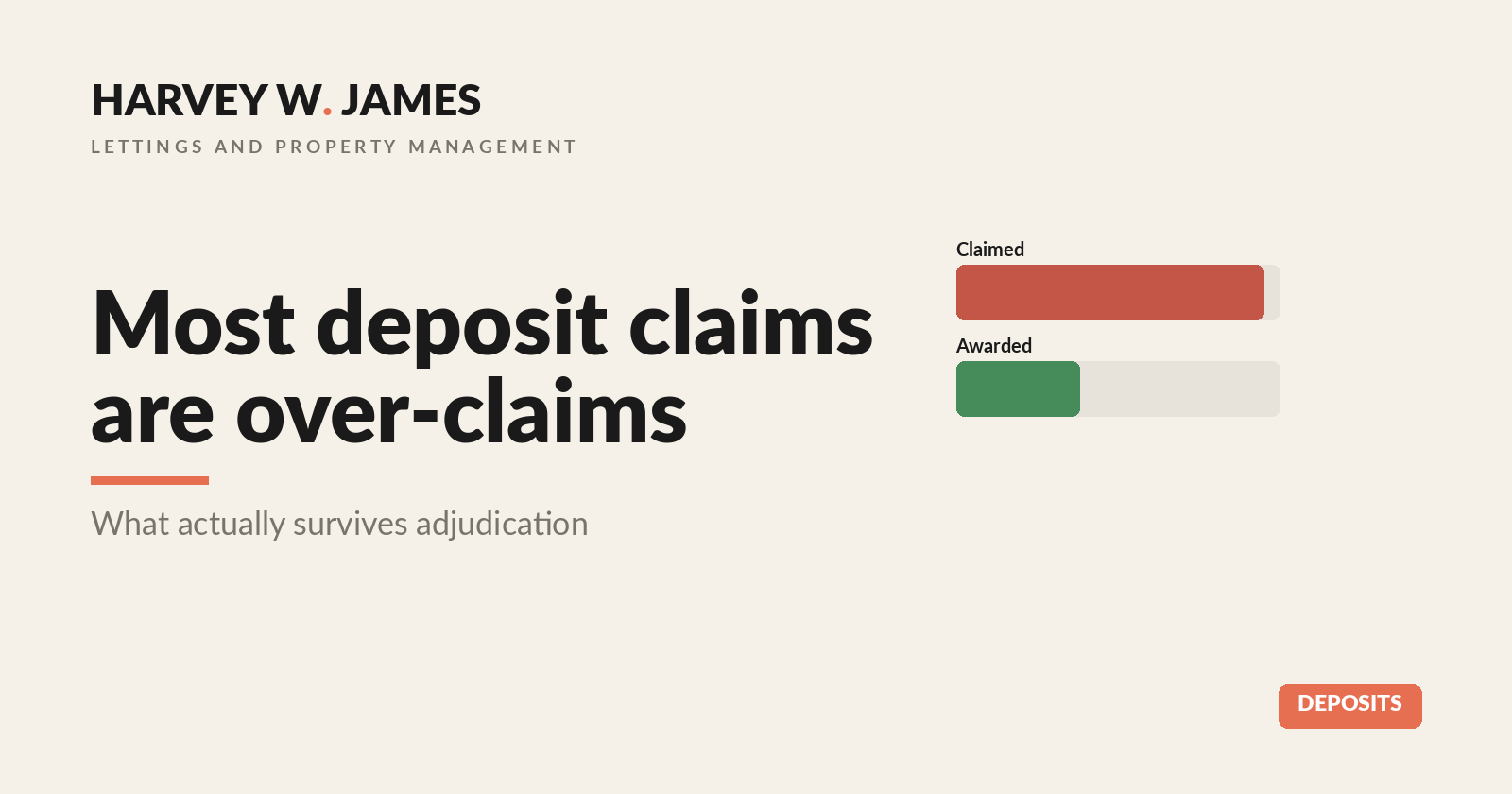

A good-quality carpet costs £500 to replace. It is four years into a ten-year life when a tenant damages it beyond repair. Most agents would put the full £500 to the tenant. An adjudicator would award around £300, because the tenant cannot be charged new-for-old: four of its ten years had already gone to fair wear, leaving six years of life that the damage destroyed. The gap between those two numbers is the single most common reason deposit claims fail, and it is the reason we assess every deduction the way an adjudicator would before any figure reaches the tenant.

The blank form is the problem

The standard end-of-tenancy process across the lettings industry is a deposit-return form. The landlord lists what they want to claim, totals up the full cost of every repair and replacement, and signs it. That total is the first figure the tenant ever sees, and it is almost always too high. It charges new-for-old, makes no allowance for the years of life already used out of a carpet, a sofa or a coat of paint, and treats normal wear as if it were damage.

Aiming high feels safer to a landlord than reducing their own claim. It is the opposite. The tenant looks at an obviously inflated number and rejects it. The claim goes to the deposit scheme's free adjudication service, an independent adjudicator applies a small set of fixed rules, and the award comes back as a fraction of the headline figure. The landlord recovers less than an accurate claim would have secured, the money has taken weeks longer to return, and the relationship with the tenant has been damaged by a number that was never realistic.

The rules an adjudicator actually applies

Deposit disputes are decided by the same handful of rules, in the same order, almost every time. Knowing them is the whole game.

The burden of proof sits with the landlord and the agent, never the tenant. The tenant does not have to prove the property was fine; the claiming party has to prove it was not, that the tenant caused the problem, and that a real cost follows. The standard is the balance of probabilities, which is a lower bar than certainty but still needs evidence rather than assertion. A dated check-in photograph set against a dated check-out photograph proves a point; a statement that the tenant "must have" caused something proves nothing.

Then there is the rule that catches most claims: no betterment. A landlord cannot replace a worn item at the tenant's expense and pocket the upgrade. Every replacement claim is reduced to reflect the age, quality and remaining life of the item at checkout. And the decision is made only on the evidence submitted, so a contractor's finding that is described but not attached, or a photograph taken but left out of the report, simply does not exist as far as the adjudicator is concerned.

Fair wear and tear, betterment, and the depreciation sum

Three ideas do most of the work in any honest assessment.

Fair wear and tear is the deterioration that comes from normal use, and it can never be charged to the tenant. How much to allow depends on the age and quality of the item at the start, its expected lifespan, how many people lived there, and how long the tenancy ran.

Betterment is the principle that the tenant cannot be made to leave the property in a better state than they found it. New-for-old is betterment.

Apportionment is the sum that puts the first two into practice. Where an item is genuinely damaged beyond fair wear and tear and has to be replaced, you take its expected lifespan, work out how much life was left at checkout, and charge the tenant only that proportion of the replacement cost. A carpet with a ten-year life, damaged five years in, yields about half its replacement cost. The same carpet damaged nine years in yields very little, and one already past its expected life yields nothing at all, because it was due for replacement anyway.

Repairs are different from replacements. A genuine repair, properly itemised, usually recovers its full reasonable cost, because mending something does not leave the landlord better off. It is the full-replacement and full-redecoration claims that collapse.

How we do it differently

The reason the industry process breaks down is sequencing: the landlord's over-claim reaches the tenant before anyone has applied any of these rules. We reverse the order.

We assess each proposed deduction first, against the independent check-in and check-out reports and the real cost of the work. We apply fair wear and tear, betterment and apportionment to reach the figure an adjudicator would award. Then we put that item-by-item position to the landlord, with the realistic figure and the reasoning, so their expectations are set on the evidence. Only then does a number go to the tenant, and by that point it is already adjudicator-grade, with the depreciation and the wear allowance shown in their favour.

Calibrating the landlord first is not working against them. It secures the most they can realistically recover, and the transparent, fully-reasoned figure is far more likely to be agreed without a dispute. We will also tell a landlord, in writing, when a deduction will not stand, because advising against a doomed claim is the advice that protects them.

This is not a matter of opinion or instinct. Every Harvey W James tenancy is documented at both ends by an independent inventory clerk, and our internal standard is built from the deposit schemes' own adjudicator best-practice guidance together with a review of dozens of real adjudications that showed us precisely where claims are won and lost. The figure we advise is the figure the adjudicator would reach, which is why almost none of our deposits reach one.

Where to look next

- Deposit Returns, Done Properly — the full operational standard, the four adjudicator rules, and the lifespan method.

- Aftercare — director-level review of high-value works and deductions before they reach a statement.

- Landlords — the full landlord proposition, fees and service tiers.

- New build deposit claim clauses — the tenancy clauses that make communal-bill recovery work at adjudication.

Sources

- TDS Guide to Inventories, Check-in and Check-out Reports — the adjudicator best-practice standard.

- Housing Act 2004 — deposit protection.

- Tenant Fees Act 2019 — the deposit cap.

- Renters' Rights Act 2025 — the regime under which the tenancy ends.

- Harvey W James Deposit Adjudication Playbook — our internal standard, built from anonymised real adjudications and the TDS guidance.

Disclaimer

This article describes the operational standard Harvey W James Ltd applies when assessing deposit deductions. It is general information about how we work, not legal advice, and not a guarantee of any outcome in an individual case. Fair wear and tear, betterment and apportionment depend on the specific facts and evidence of each tenancy, and deposit disputes are decided independently by the relevant government-approved scheme on the evidence submitted. For a specific situation, take independent advice. Cross-checked against Essential Terms and Charges v2.1.5.